Critical Illness Insurance Market Outlook 2031: Strategic Analysis and Global Trends

The global healthcare landscape is undergoing a radical transformation as the prevalence of lifestyle related chronic conditions continues to rise. Consequently, the critical illness insurance market is witnessing a significant surge in demand. By 2031, this sector is projected to reach new heights, driven by increasing healthcare costs, an aging global population, and a heightened awareness of financial security. This market analysis explores the evolving dynamics, the competitive environment, and the strategic shifts that will define the industry over the next decade.

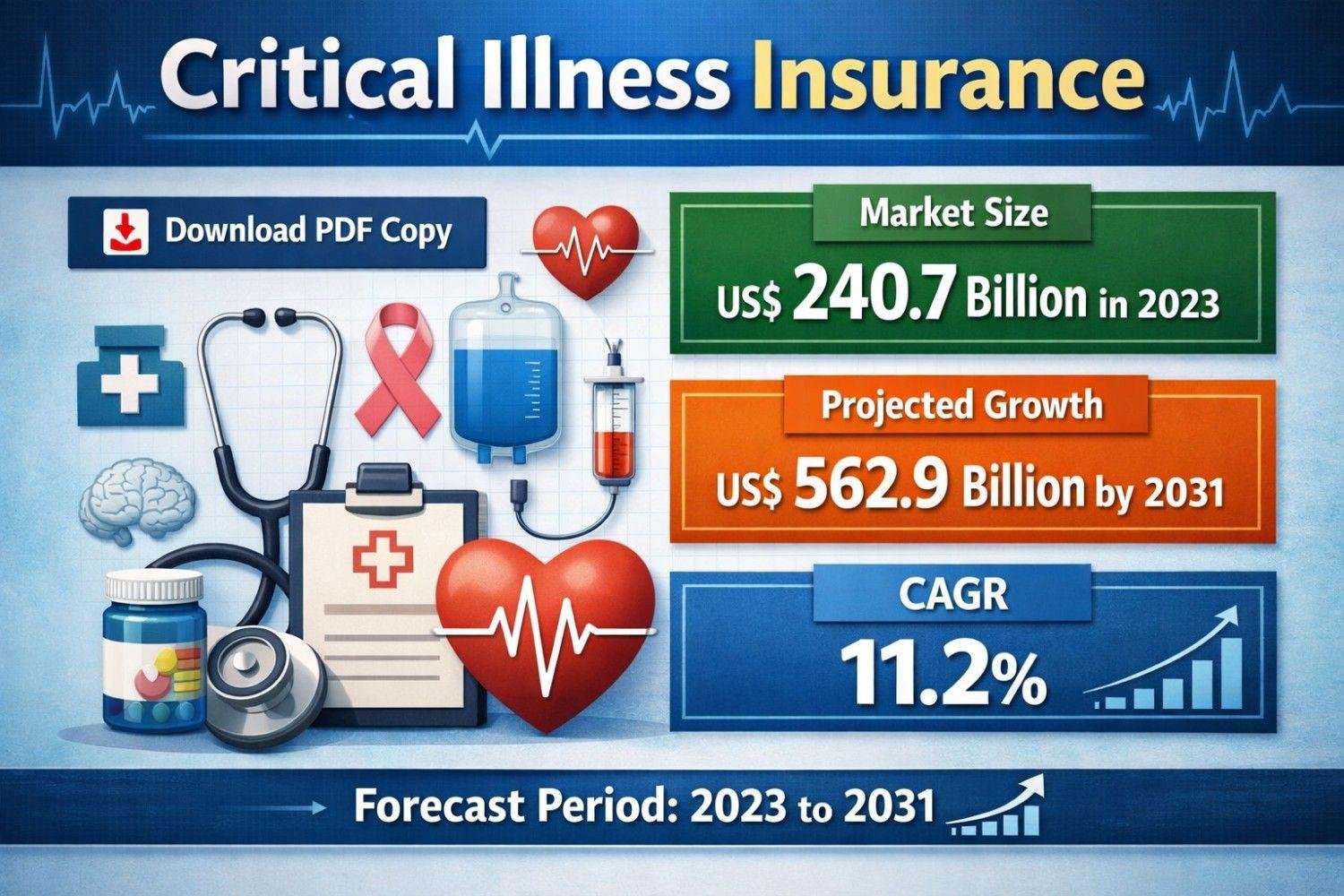

Market Analysis and Growth Drivers

Critical illness insurance Market Analysis provides a lump sum payment to policyholders upon the diagnosis of specific life threatening conditions such as cancer, heart attack, stroke, or kidney failure. Unlike traditional health insurance that covers medical expenses directly, these policies offer financial liquidity to manage non medical costs, lost wages, and specialized treatments.

The primary driver for market expansion through 2031 is the escalating cost of advanced medical technology and long term care. As medical science evolves, survival rates for critical conditions are improving, but the cost of staying alive and managing recovery is becoming more expensive. Individuals are increasingly recognizing that standard health insurance is often insufficient to cover the total economic impact of a major health crisis.

Furthermore, the corporate sector is playing a pivotal role in market growth. Many employers are now including critical illness coverage as a voluntary benefit in their employee wellness packages. This trend is particularly strong in North America and Europe, where companies utilize comprehensive benefits to attract and retain top talent. In emerging economies throughout Asia Pacific, a growing middle class with higher disposable income is seeking better financial protection, making this region a high growth pocket for insurers.

Competitive Landscape and Top Players

The competitive environment of the critical illness insurance market is characterized by a mix of established multinational insurance giants and agile insurtech startups. Companies are increasingly focusing on product differentiation by expanding the list of covered illnesses and offering flexible premium structures.

Strategic partnerships and digitalization are the two main pillars of competition. Top players are investing heavily in AI driven underwriting and digital claims processing to enhance user experience. By 2031, the market will likely see more personalized policy offerings based on individual risk profiles and genetic predispositions.

Download Sample PDF Report@ https://www.theinsightpartners.com/sample/TIPRE00011932

Top Players in the Critical Illness Insurance Market:

- Allianz SE: Known for its global reach and diverse portfolio, Allianz continues to lead by integrating digital health services with traditional coverage.

- Axa SA: Axa focuses on comprehensive health ecosystems, providing policyholders with access to second opinions and recovery support.

- Prudential Financial, Inc.: This player remains a dominant force in the North American market, focusing on simplified issuance and group benefit plans.

- MetLife Services and Solutions, LLC: MetLife excels in the employer sponsored insurance segment, offering scalable solutions for large enterprises.

- Ping An Insurance Company of China, Ltd.: As a leader in the Asian market, Ping An leverages advanced technology and a massive data pool to offer competitive pricing.

- Aflac Incorporated: Aflac remains a household name in supplemental insurance, emphasizing quick claims processing and direct to consumer marketing.

- Liberty Mutual Insurance: Liberty Mutual focuses on customizable options that allow policyholders to tailor coverage to their specific family medical histories.

Product Innovation and Rewriting the Consumer Experience

The industry is currently rewriting its approach to consumer engagement. Historically, critical illness insurance was seen as a complex and rigid product. However, the next decade will be defined by "modular" insurance. Consumers will have the ability to pick and choose specific illness buckets, such as cardiovascular or neurological packages, rather than paying for a one size fits all policy.

Additionally, the integration of wellness incentives is reshaping the market. Insurers are now offering premium discounts for policyholders who maintain healthy lifestyles, tracked via wearable devices. This shift from a purely reactive model to a proactive, health management model is expected to reduce claim frequencies while increasing customer loyalty.

Geographically, while North America currently holds the largest market share, the Asia Pacific region is expected to exhibit the highest compound annual growth rate. Rapid urbanization and the lack of comprehensive state funded social security in countries like India and Indonesia are creating a vacuum that private insurers are eager to fill.

Future Outlook

The trajectory for the critical illness insurance market remains highly positive as we head toward 2031. The integration of telemedicine and digital health consultations into insurance packages will become standard, providing a holistic value proposition beyond a simple cash payout. We expect to see a greater focus on "early stage" critical illness coverage, where payouts are triggered by early detection rather than just terminal or advanced stages of a disease. This evolution will align insurance more closely with modern preventative medicine. As financial literacy improves globally, critical illness insurance will transition from a niche supplement to a core component of a comprehensive financial plan.

Frequently Asked Questions

What is the difference between critical illness insurance and regular health insurance?

Regular health insurance generally pays for medical bills, hospital stays, and doctor fees directly to the provider. Critical illness insurance provides a lump sum cash payment directly to the policyholder upon diagnosis of a covered condition. This money can be used for any purpose, including mortgage payments, travel for treatment, or replacing lost income.

Which illnesses are typically covered in these policies?

While coverage varies by provider, most policies cover major conditions such as cancer, heart attack, stroke, organ transplants, and renal failure. Newer, more comprehensive policies may also include coverage for Alzheimer’s disease, Parkinson’s disease, and multiple sclerosis.

How does the premium for critical illness insurance work?

Premiums are usually determined based on the applicant's age, medical history, smoking status, and the amount of coverage selected. Many insurers offer "level premiums," which remain the same throughout the life of the policy, or "attained age premiums," which increase as the policyholder gets older.

The Insight Partners provides comprehensive syndicated and tailored market research services in the healthcare, technology, and industrial domains. Renowned for delivering strategic intelligence and practical insights, the firm empowers businesses to remain competitive in ever-evolving global markets.

• Email: sales@theinsightpartners.com

• Website: theinsightpartners.com

• Phone: +1-646-491-9876

Also Available in: Korean|German|Japanese|French|Chinese|Italian|Spanish