The 4.0% CAGR Paradigm: How EPR Legislation and Circularity are Scaling Textile Machinery

The global textile waste recycling machine market is entering a pivotal phase of industrialization, scaling up from localized shredding plants into highly sophisticated, automated recycling ecosystems. Pushed by the global pushback against fast fashion, the enforcement of strict Extended Producer Responsibility (EPR) frameworks, and substantial technical breakthroughs in fiber-to-fiber recovery, industrial processing machinery is experiencing steady, long-term capital deployment.

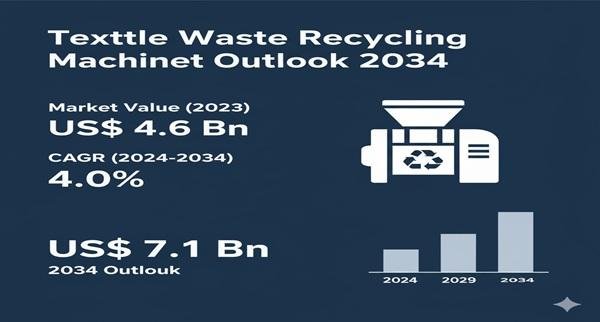

The global industry was valued at US$ 4.6 Billion in 2023 and is expected to grow at a CAGR of 4.0% from 2024 to 2034, marching toward a market value of US$ 7.1 Billion by the end of 2034.

- Primary Market Drivers: Circular Mandates and Automation

The steady trajectory toward US$ 7.1 Billion is anchored by evolving global trade parameters and a shifting manufacturing landscape:

- Aggressive EPR and Landfill Legislation: Legislative frameworks—most notably the European Union’s Waste Framework Directive—are legally forcing the separate collection and processing of post-consumer textiles. With non-compliance penalties climbing significantly, fashion brands and waste-management firms are heavily funding massive sorting and tearing machinery infrastructure.

- The AI-Powered Sorting Revolution: Sorting has historically been the industry's biggest operational bottleneck due to manual fabric identification errors. The modern integration of AI-driven optical sorting systems (such as near-infrared spectroscopy) allows processing lines to instantly separate fabrics by fiber composition, drastically reducing contamination before shredding.

- The Circular Fashion Push: Major apparel companies are setting strict internal targets to integrate recycled content into new collections. This has transformed textile recycling machinery from a niche downcycling tool (for low-value insulation and rag production) into a vital element of "closed-loop" fiber-to-fiber manufacturing.

- Machine Type & Operational Segment Highlights

The hardware composition of the market reflects both the historical backbone and the future scaling potential of textile reclamation:

- Mechanical Recycling Continues to Lead: Mechanical systems—encompassing industrial shredders, garnett machines, and fiber openers—accounted for the dominant market share in 2023. These systems remain the primary choice for medium-scale recycling due to their lower capital requirements and exceptional efficiency in shredding pure cotton, denim, and wool waste.

- Chemical Recycling Machinery Accelerates: While mechanical recycling can degrade fiber length, chemical recycling machines are expanding at the fastest growth rate. These advanced units break down complex blended fabrics (like polyester-cotton matrices) into base monomers or pure polymers, synthesizing virgin-quality recycled fibers that appeal directly to premium fashion lines.

- Mid-Capacity Operational Dominance: Processing machines featuring throughput capacities up to 2,000 kg/h lead the market. This operational footprint offers the optimal balance between initial investment costs and modular processing flexibility, making it highly attractive to localized textile-recycling hubs globally.

- Regional Dynamics: Global Production and Consumption Hubs

- Asia-Pacific (The Manufacturing Epicenter): Asia-Pacific commands the absolute majority of global revenue. Driven by the colossal textile footprints of China and India, regional manufacturers are building out large-scale machinery setups to handle immense pre-consumer cutting scraps and post-industrial textile waste directly at the source.

- Europe (The Regulatory Pioneer): Fueled by progressive zero-waste mandates and massive public-private green investments in countries like France and Germany, Europe serves as the premier testing ground for high-throughput automated processing lines and closed-loop technologies.

- North America: The market here is scaling up rapidly through localized waste-diversion strategies. Heightened consumer awareness regarding fast-fashion waste, alongside new localized legislative pushes like California’s SB 707, is accelerating brand partnerships with industrial recycling yards.

Challenges Restraining the Market

Despite a strong regulatory wind, the market faces clear financial bottlenecks. High upfront capital costs for fully automated sorting lines and multi-stage chemical depolymerization reactors present a steep barrier to entry for small and mid-sized operators. Operationally, processing mixed-fabric blends (such as elastane/spandex blends) remains a technical hurdle, requiring complex chemical pre-treatments that increase energy consumption and overall maintenance overhead. This keeps the industry heavily reliant on consistent feedstocks to maintain reliable profit margins.